July job openings increased to 10.9 million, up 779,000 from June. The record number suggests weaker August job growth was partly related to a low supply of workers and demand for workers remains robust.

Key Points for the Week

- July job openings increased to 10.9 million, indicating demand for workers remains high.

- The European Central Bank scaled back the size of its bond purchases but remains committed to keeping rates low.

- President Biden and Chinese President Xi discussed U.S.-Chinese relations.

European economic growth isn’t vigorous, but it has improved enough for the European Central Bank to scale back its bond purchases. Inflation pressures also spurred the ECB to tweak its policies. Consumer inflation in China remains dormant, increasing only 0.8% in the last year. Producer prices in the U.S. and China surged 8.3% and 9.5% respectively as input costs continue to increase globally amid supply shortages and resurgent demand.

Stocks retreated on concerns about the economy slowing because of COVID-19 resurgences. The S&P 500 shed 1.7%. The MSCI ACWI slid 1.2%. The Bloomberg U.S. Aggregate Bond Index was roughly unchanged. U.S. and Chinese retail sales data, along with U.S. consumer data, headline key releases this week.

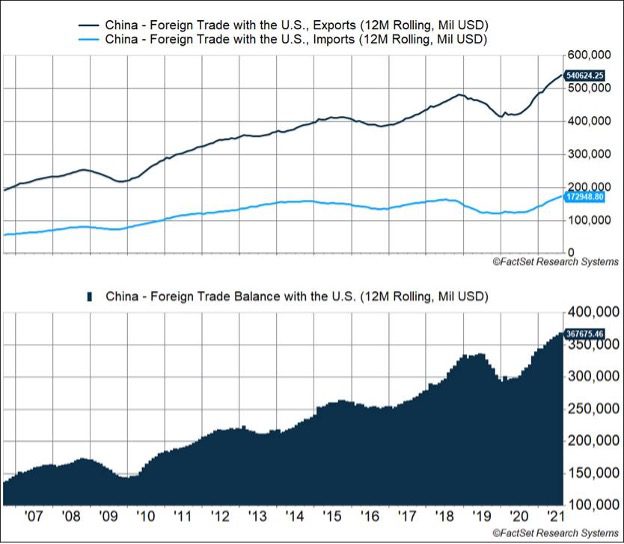

Figure 1

Reach Out and Touch Someone

In the 80s, a popular advertisement for long-distance phone calls encouraged people to “reach out and touch someone” to keep in close contact. Last week, U.S. President Joe Biden and Chinese President Xi Jinping did just that by holding their first phone call in seven months. The leaders of the world’s two largest economies had “a broad strategic discussion” on economic issues, climate change, and COVID-19.

Phone calls like these are used to reassure the public that both presidents are working to resolve some of the challenges between the two countries. Investors should pay close attention as many leading companies may be affected by changes in the relationship between the two economic giants.

China has been listed as a top five risk in our quarterly market outlook for most of the last three years. The relationship between the U.S. and China has become more competitive and tense in recent years, primarily because of a lingering trade imbalance. As Figure 1 shows, the trade deficit between the U.S and China continues to widen. U.S economic stimulus efforts have likely contributed by encouraging U.S. consumers to purchase more goods during the pandemic. Invariably, some of those goods were manufactured in China.

Other issues are also potential risks:

- Climate change and how much each country is willing to cut back activity to reduce emissions

- Continued uncertainty around the source of COVID-19

- S. pressure on its allies not to use Chinese technology

- China’s persecution of minorities

- China’s more aggressive foreign policy in contrast to the U.S. stepping back from global commitments

In recent months, China has signaled an authoritarian turn in its approach to economic issues. The Chinese government has made clear that corporations need to follow Beijing’s lead. In June, China’s largest ride-hailing company went public in the U.S. Chinese officials had expected the company to delay its offering. In response, China put the company under a cybersecurity review and banned it from accepting new users. Earlier, a Chinese financial company was forced to call off its IPO because of government pressure.

China is also tightening internet regulation. The country recently announced more stringent rules governing how internet companies can use personal data. It even went so far as to ban online lists that rank celebrities by popularity and to limit wasteful spending on endorsed goods. Perhaps the most drastic change is China’s move to limit video game playing to three hours per week for individuals under 18.

The investment implications from U.S-Chinese relations and changes inside China will play out for years to come. In the near term, the growing trade deficit and potential policy changes raise the risk of reigniting the trade war between the two countries. The Chinese also seem to be leaning toward tighter regulation of companies and information. While gaming restrictions may provide China with better-educated citizens more able to compete effectively in the world, they may also undercut Chinese game designers from competing in a rapidly growing industry.

One of the downsides to covering market information on a weekly basis is it becomes easier to miss the forest for the trees. None of the issues in this week’s update warranted a major analysis in the week they happened, but collectively they suggest China is adjusting its approach to issues likely to affect the global economy in coming years.

—

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://www.wsj.com/articles/didi-ipo-china-regulators-investors-trouble-11625873909

https://supchina.com/2021/09/09/idol-worship-and-fan-culture-in-china-explained/

https://www.wsj.com/articles/china-passes-one-of-the-worlds-strictest-data-privacy-laws-11629429138

https://clickamericana.com/media/advertisements/reach-out-reach-out-and-touch-someone-1979-1982

Compliance Case #01130940